Factors affecting the economic growth of Organization of Islamic Cooperation (OIC) member countries

DOI:

https://doi.org/10.29244/hass.2.2.37-41Keywords:

Economic growth, Oranization of Islamic Cooperation (OIC), Panel data, Population, Working-age populationAbstract

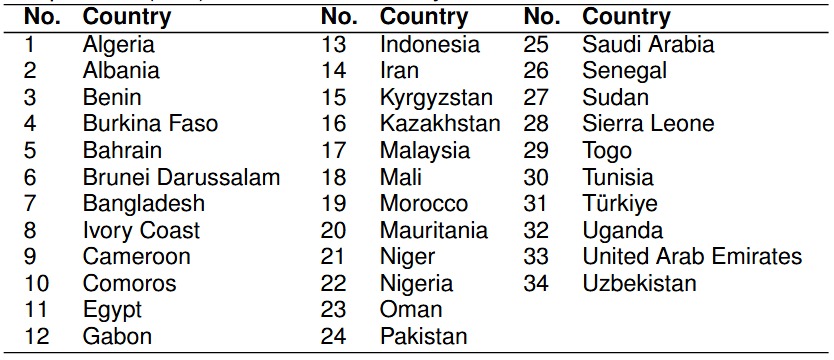

Economic growth is widely used as a macroeconomic indicator for describing economic performance and, by extension, shifts in material living standards. Therefore, this study centers on the Organization of Islamic Cooperation (OIC), an international forum with predominantly Muslim member states, and examines the relationship between selected macroeconomic variables and economic growth across OIC countries from 2000 to 2021, a timeframe marked by two major global economic crises. In order to achieve the stated objective, panel data regression was applied to observations from 34 countries with complete data on inflation, net exports, gross fixed capital formation, real interest rates, working-age population, and total population. Panel regression was estimated under the Common Effects Model (CEM), Fixed Effects Model (FEM), and Random Effects Model (REM), with model selection based on specification tests. The Chow test (F = 167.4303; p = 0.0000) and Hausman test (² = 101.8431; p = 0.0000) consistently support the FEM as the preferred model. FEM results indicate that inflation and the real interest rate negatively and significantly affect GDP (INF: β = 0.007252, p = 0.0000; RIR: β = 0.008265, p = 0.0000), while net exports, gross fixed capital formation, working-age population, and population positively and significantly influence GDP (LnNetExp: β = 0.228393, p = 0.0000; LnGFC: β = 0.321654, p = 0.0000; PAK: β = 0.007255, p = 0.0104; LnPOP: β = 0.790510, p = 0.0000). All variables are jointly significant (F-statistic = 6735.187; p = 0.0000), and the model exhibits very high explanatory power (R² = 0.997722; adjusted R² = 0.997574). The findings underscore the critical role of price stability and real borrowing costs, alongside trade performance, capital accumulation, and demographic–labor dynamics, in shaping growth trajectories across OIC economies.

References

Akalpler E, Shamadeen B. The role of net export on economic growth in the United States of America. J Appl Econ Sci. 2017;12(3):772-781.

Ali G. Gross fixed capital formation & economic growth of Pakistan. J Res Humanit Arts Lit Appl. 2015;1(2):21-30.

Aydın C, Esen Ö, Bayrak M. Inflation and economic growth: a dynamic panel threshold analysis for Turkish republics in transition process. Procedia-Social and Behavioral Sciences. 2016;229:196-205. https://doi.org/10.1016/j.sbspro.2016.07.129 DOI: https://doi.org/10.1016/j.sbspro.2016.07.129

Bakare AS. A theoretical analysis of capital formation and growth in Nigeria. Far East Journal of Psychology and Business. 2011;3(2):11-24.

Bawazir AAA, Aslam M, Osman AFB. Demographic change and economic growth: empirical evidence from the Middle East. Econ Chang Restruct. 2020;53(3):429-450. https://doi.org/10.1007/s10644-019-09254-8 DOI: https://doi.org/10.1007/s10644-019-09254-8

Cili MR, Alkhaliq B. Economic growth and inflation: evidence from Indonesia. Signifikan: Jurnal Ilmu Ekonomi. 2022;11(1):145-160. https://doi.org/10.15408/sjie.v11i1.19848 DOI: https://doi.org/10.15408/sjie.v11i1.19848

D'Adda C, Scorcu AE. Real interest rate and growth: an empirical note. Bologna: University of Bologna; 1997. Available at: http://amsacta.unibo.it/764/1/276.pdf

Eidoo S. The Organization of Islamic Cooperation, ummah unity and children's rights to education. In: Daun H, Arjmand R, editors. Handbook of Islamic Education. Cham: Springer International Publishing; 2017. pp. 1-21. https://doi.org/10.1007/978-3-319-53620-0_9-1 DOI: https://doi.org/10.1007/978-3-319-53620-0_9-1

Furuoka F. Population and economic development in Indonesia: a revisit with new data and methods. Acta Oeconomica. 2013;63(4):451-467. https://doi.org/10.1556/aoecon.63.2013.4.3 DOI: https://doi.org/10.1556/aoecon.63.2013.4.3

Gujarati DN, Porter DC. Basic Econometrics. 5th ed. New York: McGraw-Hill; 2009.

Gunawan MH. Pertumbuhan ekonomi dalam pandangan ekonomi Islam. Jurnal Tahkim. 2020;XVI(1):117-128.

Hansen BE, Seshadri A. Uncovering the relationship between real interest rates and economic growth. Michigan Retirement Research Center Research Paper No. 2013-303. 2013. https://doi.org/10.2139/ssrn.2391449 DOI: https://doi.org/10.2139/ssrn.2391449

Jordaan AC, Eita JH. Export and economic growth in Namibia: a Granger causality analysis. South African J Econ. 2007;75(3):540-547. https://doi.org/10.1111/j.1813-6982.2007.00132.x DOI: https://doi.org/10.1111/j.1813-6982.2007.00132.x

Khan MS, Reinhart CM. Private investment and economic growth in developing countries. World Dev. 1990;18(1):19-27. https://doi.org/10.1016/0305-750X(90)90100-C DOI: https://doi.org/10.1016/0305-750X(90)90100-C

Kurniawati V. Analysis the impact of net export, investment, labour and exchange rate on economic growth in Indonesia in the year of 2000-2020. Jurnal Akuntansi, Manajemen dan Ekonomi. 2021;23(2):40-50.

Kusumatrisna AL, Sugema I, Pasaribu SH. Threshold effect in the relationship between inflation rate and economic growth in Indonesia. Bulletin of Monetary Economics and Banking. 2022;25(1):117-132. https://doi.org/10.21098/bemp.v25i1.1045 DOI: https://doi.org/10.21098/bemp.v25i1.1045

Malthus TR, Stimson S. An Essay on the Principle of Population. New Haven: Yale University Press; 2018. https://doi.org/10.12987/9780300231892 DOI: https://doi.org/10.12987/9780300231892

Mamo FT. Economic growth and inflation: a panel data analysis. Economics. 2012.

Mankiw NG. Makroekonomi. 6th ed. Jakarta: Penerbit Erlangga; 2007.

Mankiw NG. Principles of Macroeconomics. 8th ed. Boston: Cengage Learning; 2018.

Meyer DF Sanusi KA. A Causality Analysis Of The Relationships Between Gross Fixed Capital Formation, Economic Growth And Employment In South Africa. Studia Universitatis Babes-Bolyai Oeconomica. 2019;64(1):33-44. https://doi.org/10.2478/subboec-2019-0003 DOI: https://doi.org/10.2478/subboec-2019-0003

Mulyadi. Akuntansi Biaya. 5th ed. Yogyakarta: Universitas Gadjah Mada; 2014.

Musa A. Econometric model on population growth and economic development in India: an empirical analysis. Proceedings of the International Symposium on Emerging Trends in Social Science Research, Chennai-India. 2015. pp. 3-5.

Ncanywa T, Makhenyane L. Can investment activities in the form of capital formation influence economic growth in South Africa?. Proceedings of SAAPAM Limpopo Chapter 5th Annual Conference Proceedings. 2016. p. 270-279.

Parakkasi I. Analisis dampak suku bunga terhadap pertumbuhan sektor riil dan sektor investasi dalam perspektif syariah di Kota Makassar. LAA MAISYIR: Jurnal Ekonomi Islam. 2016;7(2):161-180.

Pazim KH. Panel data analysis of "export-led" growth hypothesis in BIMP-EAGA countries. Univ Libr Munich, Ger MPRA Pap. 2009.

Phillips AWH. Employment, inflation and growth. London: Bell; 1962. https://doi.org/10.2307/2601516 DOI: https://doi.org/10.2307/2601516

Purnomo RA. 2016. Analisis statistik ekonomi dan bisnis dengan SPSS. Ambarwati PC, editor. Ponorogo: CV. Wade Grup; 2016.

Raghutla C, Chittedi KR. Is there an export- or import-led growth in emerging countries? A case of BRICS countries. Journal of Public Affairs. 2020;20(3):1-12. https://doi.org/10.1002/pa.2074 DOI: https://doi.org/10.1002/pa.2074

Rahman MM. Impact of labour force participation on economic growth in South Asian countries. United International University; 2018. Available at: https://www.iiste.org

Rinaldi M, Jamal A, Seftarita C. Analisis pengaruh perdagangan internasional dan variabel makro ekonomi terhadap pertumbuhan ekonomi Indonesia. J Ekon dan Kebijak Publik Indones. 2017;4(1):49-62.

Saputra RD, Rusdi M. Analysis of factors affecting economic growth in Banten Province. EKOMBIS REVIEW: Jurnal Ilmiah Ekonomi dan Bisnis. 2024;12(1):659-666. https://doi.org/10.37676/ekombis.v12i1.4998 DOI: https://doi.org/10.37676/ekombis.v12i1.4998

Sebikabu DR, Ruvuna E, Ruzima M. Population growth's effect on economic development in Rwanda. In: Das GG, Johnson RB, editors. Rwandan Economy at the Crossroads of Development: Key Macroeconomic and Microeconomic Perspectives. Singapore: Springer Singapore; 2020. p. 73-95. https://doi.org/10.1007/978-981-15-5046-1_5 DOI: https://doi.org/10.1007/978-981-15-5046-1_5

Suciany AD, Damayanti CR, Darmawan A. Exchange rate, inflation, interest rate and economic growth: how they interact in ASEAN. Profit: Jurnal Administrasi Bisnis. 2024;18(2):245-256.

Sugiyono. Metode Penelitian Kuantitatif, Kualitatif dan R&D. Bandung: CV. Alfabeta; 2017.

Sutarjo, Murti W, Saleh S. The effect of export import, inflation, interest rates, and exchange rates against Indonesia's economic growth. International Journal Business, Economics & Management. 2021;4(2):449-460.

Tambunan T. Perekonomian Indonesia: kajian teoritis dan analisis empiris. Jakarta: Ghalia Indonesia; 2011. Available at: https://books.google.co.id/books?id=M-dAtwAACAAJ

Ugochukwu US, Chinyere UP. The impact of capital formation on the growth of Nigerian economy. Research Journal of Finance and Accounting. 2013;4(9):36-43.

Ullah S, Bedi-uz-Zaman, Farooq M, Javed A. Cointegration and causality between exports and economic growth in Pakistan. European Journal of Social Science. 2009;10(2):264-272.

Umar H. Dampak krisis sub-prime mortgage terhadap ekonomi makro dan pasar modal di Indonesia. JRB-Jurnal Riset Bisnis. 2017;1(1):8-18. https://doi.org/10.35592/jrb.v1i1.4 DOI: https://doi.org/10.35592/jrb.v1i1.4

Widarjono. Ekonometrika Teori dan Aplikasi untuk Ekonomi dan Bisnis. Yogyakarta: Ekonisia; 2018.

Published

Issue

Section

License

Copyright (c) 2025 Ahmad Fauzan, Mohammad iqbal Irfany

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

How to Cite